Cyber Fraud in India: How Scams Actually Work and How to Protect Yourself

Olivia Bennett July 7, 2026 0

how they actually work and how to protect yourself.

India’s digital economy has expanded faster than most people’s understanding of the risks that come with it. Government data presented to Parliament put reported cyber fraud losses at roughly ₹22,845 crore in 2024 — a 206% jump from the previous year — and case volumes kept climbing through 2025, crossing 28 lakh reported incidents. Industry estimates that account for underreporting, which cybersecurity researchers say is significant, push the real figure considerably higher, with some projections for 2025 approaching ₹1.2 lakh crore once unreported losses are factored in.

The gap between the official, reported number and the estimated real number matters. Most victims never file a complaint — some out of embarrassment, others because they assume a small loss isn’t worth the paperwork, and many because they don’t realize a formal reporting channel even exists. Understanding how these frauds are actually engineered, rather than just memorizing generic warnings, is what separates people who spot the pattern early from people who don’t.

Table of Contents

- The Business Model Behind Cyber Fraud

- Digital Arrest Scams: A Uniquely Indian Phenomenon

- Investment Fraud: Why Even Experienced Traders Fall For It

- Why So Few Cyber Criminals Are Ever Convicted

- The OTP and Password Myths That Don’t Actually Protect You

- Securing Your Gmail Account: The Risk Most People Ignore

- Does Quantum Computing Threaten Your Bank Account?

- What to Do Immediately If You’ve Been Defrauded

- Key Takeaways

- Frequently Asked Questions

The Business Model Behind Cyber Fraud

It helps to stop picturing a lone scammer on a laptop. Large-scale cyber fraud in India runs as a division-of-labor operation, closer to a supply chain than a single crime.

- Data brokers compile and categorize personal information — who has money, who’s recently searched for loans, who’s active in a particular WhatsApp or Telegram community.

- Callers (social engineers) use that data to build trust quickly, often posing as officials, financial advisors, or customer support agents.

- Mule account and SIM providers supply the disposable bank accounts and phone numbers that make the money trail hard to follow, rotating them every few days as accounts get frozen.

- Cash-out operators move stolen funds out of a compromised account and abroad within minutes to hours, before authorities can act.

Several of these operations have physically relocated to Southeast Asia in recent years — compounds in Myanmar, Cambodia, and along the Thailand border have become notorious after reports emerged of people being lured with fake job offers, then held and forced to run scam call centers. Indian authorities, working with the Ministry of External Affairs, have coordinated rescue operations for hundreds of trafficked workers caught in these networks, though officials acknowledge many remain unaccounted for.

This is also why fraud isn’t uniquely an Indian problem, even though the country’s sheer population makes it an attractive target. The UK and Australia both report annual losses in the billions from comparable scam categories, and China’s own restrictive digital ecosystem — not an absence of criminal intent — is generally cited as the reason less fraud appears to originate domestically there.

Digital Arrest Scams: A Uniquely Indian Phenomenon

The “digital arrest” scam has become one of the fastest-growing fraud categories in the country. A caller poses as a CBI officer, customs official, or cybercrime investigator and tells the victim their Aadhaar, phone number, or bank account has been linked to a serious crime — often drug trafficking or money laundering. The victim is then kept on a continuous video call, told not to contact anyone, and warned they’ll be physically arrested the moment the call ends. Coercion can last hours, sometimes days.

Cyber law specialists have been blunt about one fact: there is no such thing as a “digital arrest” under Indian law. Every arrest requires a warrant and is carried out in person through due legal process. No investigating agency conducts an arrest, verdict, or bail process over a video call.

The numbers reflect how effective the psychological pressure has been regardless: reported digital arrest cases rose from roughly 39,925 in 2022 (with losses of about ₹91 crore) to 123,672 cases in 2024, with victims collectively losing close to ₹1,935 crore. The government has since launched an awareness campaign — including caller-tune messaging distributed by telecom operators — specifically targeting this scam type.

Investment Fraud: Why Even Experienced Traders Fall For It

Investment scams, typically run through WhatsApp or Telegram “trading tip” groups, have overtaken most other categories to become the single largest source of financial loss in Indian cyber fraud, reportedly accounting for a majority share of total money lost in 2025.

The pattern is consistent: a victim is added to a group full of other “investors” sharing screenshots of rapid profits. A fake trading dashboard shows the victim’s own money apparently growing. Early withdrawal requests are honored — often for a modest amount — specifically to build trust before larger sums are deposited. When the victim tries to withdraw a significant amount, the platform stalls, invents new “fees,” and eventually disappears entirely.

What makes this category dangerous is that market experience doesn’t inoculate anyone against it. Cases publicly reported in 2025 and 2026 include a share trader with years of genuine market experience losing nearly ₹87 lakh, and separate victims losing over ₹2 crore and ₹3 crore respectively through near-identical fake dashboard tactics. The scam isn’t exploiting ignorance of markets — it’s exploiting the same trust-building mechanics used in the “digital arrest” scam, just applied to greed instead of fear.

Why So Few Cyber Criminals Are Ever Convicted

This is the part most awareness campaigns skip, and it’s worth understanding because it explains why “just report it” isn’t as simple as it sounds.

When police do raid a known fraud hotspot — and India currently has an estimated 70-80 identified hotspot regions, with Jharkhand’s Jamtara district being the most widely publicized — they typically recover dozens of accounts and SIM cards. But the accounts linked to any single victim’s complaint are usually already frozen or abandoned by the time an arrest happens, and the SIM card used is often already discarded. Investigators then face a mapping problem: proving in court that the specific person arrested is the same person who made a specific fraudulent transaction, when the paper trail runs through accounts registered to unrelated third parties whose identity documents were stolen or bought.

Adding to the difficulty, fraudsters deliberately fragment stolen money across dozens or hundreds of accounts in small increments — sometimes as little as ₹300–500 per transfer — specifically because each frozen account requires separate legal action to recover funds, and by the time all of them are processed, much of the money has already been withdrawn as cash. Recent data suggest the fund-freezing and recovery rate has been improving — Delhi Police reported freezing roughly 20% of defrauded funds in 2025, double the prior year’s rate — but nationally, the majority of victims still don’t recover their losses even when the fraudster is eventually caught.

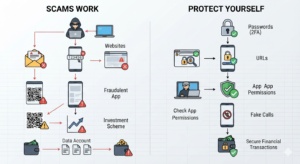

The OTP and Password Myths That Don’t Actually Protect You

Public awareness campaigns in India have relentlessly repeated a handful of messages: don’t share your OTP, use a complex password, check for “https” in a link. These aren’t wrong, exactly, but they miss the more important point.

- Fraudulent websites use HTTPS too. A criminal has no incentive to build an insecure-looking site; encryption certificates are free and instant to obtain, and using one only makes a scam look more legitimate.

- Password complexity doesn’t stop credential theft. No amount of complexity protects a password that a victim is socially engineered into typing directly into a fake site or reading aloud over a call.

- The real risk is over-reliance on OTP as the only real barrier, precisely because it’s the one thing every awareness campaign focuses on — leaving people under-prepared for scenarios where an OTP isn’t even the weak point (screen-recording, call forwarding tricks, or fake customer-support numbers requesting a “verification code” for an unrelated purpose).

Globally, many digital ecosystems are shifting toward OTP-less, passkey-based authentication precisely because SMS-based one-time codes have proven easy to socially engineer at scale. Until that transition is complete in India, the safest habit isn’t just “don’t share the OTP” — it’s treating any unsolicited request for one, regardless of the reason given, as an automatic red flag.

Securing Your Gmail Account: The Risk Most People Ignore

Most personal and financial identity in India now funnels through a single Gmail account — banking alerts, photos, saved passwords, and increasingly, government services. Yet the biggest practical risk isn’t a sophisticated remote hack; it’s a Gmail session left logged in on a device you’ve forgotten about.

A few concrete habits close most of this gap:

- Enable two-factor authentication, but understand its limits — 2FA alone doesn’t help if a device is already logged in.

- Audit every device connected to your account through Gmail’s security settings periodically, and sign out of any laptop, tablet, or old phone you no longer actively use.

- Treat Google backup codes as spare OTPs, not disposable text. These codes allow account recovery without your phone in hand — useful if your device is lost or stolen, but a serious liability if anyone else accesses them, since each one can be used to log in exactly like a real OTP.

- Never log into personal accounts on shared or public devices, including print shops and cyber cafés — a surprisingly common source of real-world account compromise, since a logged-in session on someone else’s machine can allow app installation, password resets, and full dashboard access.

If you notice unexplained access to private conversations or your physical location — and ruling out a compromised device turns up nothing — it’s worth considering that the leak may not be digital at all. Investigators have handled real cases where a hidden recording device, not a hacked phone, was the actual source of a stalking victim’s compromised privacy.

Does Quantum Computing Threaten Your Bank Account?

Headlines periodically claim that quantum computers have “cracked” RSA encryption — the standard underlying most banking and internet security. This deserves a direct correction: as of now, they haven’t. A widely circulated 2024 Chinese research paper was reported by some outlets as having broken RSA-2048 encryption; independent cryptographers who reviewed it found the study had actually factored numbers as small as 22 to 50 bits — a task any laptop can already do in milliseconds — nowhere close to the 2048-bit keys used in real-world encryption. Breaking genuine RSA-2048 encryption is estimated to require thousands of stable logical qubits, a capability that remains years to decades away by most expert assessments.

That said, “not yet” isn’t the same as “never,” and the world’s cryptography standards bodies are preparing accordingly. The U.S. National Institute of Standards and Technology finalized its first post-quantum cryptography standards in 2024, based on algorithms known as CRYSTALS-Kyber and CRYSTALS-Dilithium, specifically designed to resist future quantum-based attacks. India launched its own National Quantum Mission in 2023 with a ₹6,003.65 crore budget through 2030-31, aimed at building domestic quantum computing and communication capability. For ordinary users, the practical takeaway is simple: this is a long-term infrastructure concern for banks, governments, and platform operators to manage — not a reason to change your personal security habits today.

What to Do Immediately If You’ve Been Defrauded

Speed matters more than almost anything else in cyber fraud recovery.

- Call the national cybercrime helpline, 1930, or file a complaint at cybercrime.gov.in immediately — within the first hour if possible. This is often described as the “golden hour,” since stolen funds typically move through several layers of accounts within minutes.

- Provide the exact transaction ID and amount so authorities can attempt to freeze the receiving account before funds are withdrawn or moved further down the chain.

- Don’t wait to “confirm” the fraud yourself. Victims who delay reporting to verify details themselves lose the narrow window during which a freeze is still possible.

- Follow up in writing with your bank as a parallel step, since banks also have their own fraud-reporting obligations once notified.

- Expect a process, not an instant refund. Even a successful freeze can take weeks to months to resolve if multiple victims’ claims point to the same partially recovered account, since courts may need to determine how limited recovered funds are distributed.

Key Takeaways

- Reported cyber fraud losses in India crossed ₹22,000 crore in 2024 alone, with real losses — including underreported cases — estimated considerably higher.

- Digital arrest scams have no legal basis in India; no agency arrests, questions, or holds anyone via video call.

- Investment fraud through WhatsApp and Telegram groups is now the largest single category of financial loss, and targets experienced investors just as effectively as first-timers.

- Low conviction rates stem from a structural mapping problem — mule accounts and disposable SIMs make it genuinely difficult to legally link a suspect to a specific transaction.

- Widely repeated advice like “avoid non-HTTPS links” and “use complex passwords” addresses a smaller risk than the core vulnerability: social engineering that bypasses these protections entirely.

- Leaving Gmail logged into old devices, and treating backup codes casually, is a bigger everyday risk than most sophisticated remote hacking.

- Quantum computers have not broken real-world encryption yet, despite periodic sensational claims — but global and Indian cryptography standards are already being upgraded as a precaution.

- Reporting fraud to 1930 or cybercrime.gov.in within the first hour meaningfully improves recovery chances; delay sharply reduces them.

Frequently Asked Questions

1. What is a digital arrest scam, and is it recognized under Indian law?

No. There is no legal concept of a “digital arrest” in India. Genuine arrests require a warrant and are carried out in person through due process — never through a sustained video call. Any caller claiming this authority is committing fraud.

2. Is it ever safe to share an OTP with someone who contacts me?

No legitimate bank, government agency, or service provider will ever ask you to read out or forward an OTP to them. Treat any such request — regardless of the stated reason — as a fraud attempt.

3. How can I secure my Gmail account from being compromised?

Enable two-factor authentication, regularly review and remove old devices from your account’s active sessions, avoid logging into personal accounts on shared or public computers, and store any downloaded backup codes with the same caution you’d apply to a physical OTP.

4. What should I do immediately if I’ve been a victim of online fraud in India?

Call the 1930 helpline or file a complaint at cybercrime.gov.in as fast as possible, ideally within the first hour, and provide exact transaction details so the receiving account can potentially be frozen before funds move further.

5. Can quantum computers currently break the encryption protecting my bank account?

No. Despite periodic headlines, no quantum computer has broken real-world 2048-bit RSA encryption. Cracking it at scale is estimated to require thousands of stable logical qubits, a capability most experts believe is still years to decades away. Global and Indian institutions are nonetheless already developing quantum-resistant encryption standards as a long-term precaution.

6. Why do so few cyber fraud cases in India result in a conviction?

Investigators often can’t legally link a captured suspect to a specific complaint, since the mule bank accounts and SIM cards used in a fraud are typically registered to unrelated third parties and are discarded or frozen before an arrest is made — making courtroom proof of identity a genuine structural challenge, not simply a lack of police effort.